You make me unhappy

Hello! Remember me? You sold me a shirt last year for US$10. I know there is a global financial crisis but it would be great if you can sell it to me at the same price again. How would something that happens in the West affect you? Why does it matter if inflation and interest rates are rising? How do oil prices affect your textile manufacturing? You are unhappy now? You will increase prices to US$20? This makes me very unhappy.

This is basically what happened in 2008-09 during which the world experienced an economic crisis which started with a few banks in the US and spread across the globe. Developed countries took the hardest hit but developing countries were not completely spared. It was a supply side shock since suppliers could no longer provide the same number of goods and services at the same prices as before. This was because global banks started failing and could not lend as much money at the same prices.

When you have a lot of money, it is easy to invest in risky countries like Pakistan. When money dries up, you will ask for a higher reward if you are to take the risk of investing in Pakistan. Even though Pakistani businesses do not take many loans domestically (we will discuss this later), it was facing structural issues back then as well – being a consumption-driven and investment-lacking fragile economy – and so, it suffered.

This context is good to understand what will be the economic impact of the pandemic on Pakistan’s economy.

You made yourself unhappy

We have discussed the CIGXM of the Pakistani economy which is focused on the demand side and impacts my (the buyer’s) happiness. But we have to worry about you, the seller, too. In the years before 2008, you had not been saving and hence, not investing. As soon as, 7,000 miles away, some bank went bust, your fragilities came to light.

As global oil prices rose, your input costs rose. When you went to the bank to take out a loan, they said we will charge you a higher rate. So you had to increase prices to meet the demand. That led to inflation and, consequently, even higher interest rates. We will discuss this cycle in more detail later. Point is: you became unhappy so you made me unhappy.

Some things to note on the supply side: it is made up of three main components. In order to run the factory that produces the shirt you sell, you need people who work, labor (L), and machinery that they will work with, capital (K). We are using ‘K’ here and not ‘C’ because we do not want to confuse capital with consumption.

Additionally, you also need to continually innovate and bring in the latest technology by investing in new machinery and production techniques to become more efficient. This innovation is even more important at a country level because if Pakistan’s population is increasing, our demand for goods and services will continue to rise. In order to serve this higher demand at the same prices, suppliers need to innovate or else, increase prices. This improvement in efficiency is called total factor productivity (A).

We weren’t as unhappy in 2008-09

As bad as I just made it sound, Pakistan, like other emerging markets, managed to avoid a recession during the global financial crisis. Real growth in emerging markets slowed down to positive 3% in 2009 while advanced economies actually had negative 3% growth. According to the IMF, the Great Lockdown will lead to negative growth of 5% across the world with emerging markets suffering by -3% and advanced economies by -8%.

The economic impact of the pandemic is expected to be worse this time because it is not just a supply side shock with you not going to your factory to make me the shirt I want. It is also a demand shock because I actually might not be able to afford the shirt anymore since there is a high chance I will either be out of a job or have gotten a pay cut.

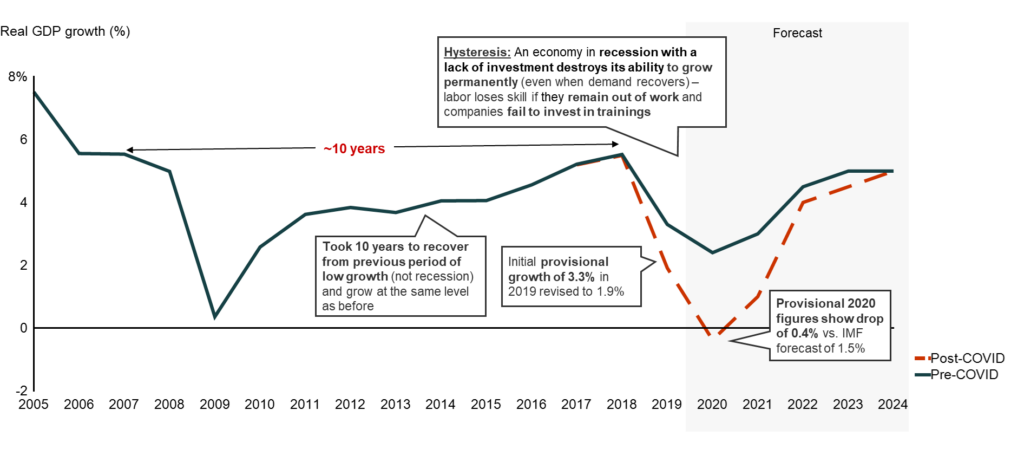

Last time, it took 10 years for the world and Pakistan to recover from the financial crisis as you can see below:

Pakistan’s real GDP growth (2005-2024)

Why the recovery took so long is because of ‘hysteresis’. I know the word is not bite-sized but the explanation is quite straightforward.

When an economy in slowing down, the lack of investment destroys its ability to grow permanently (even when demand recovers) – labor loses skill if they remain out of work and companies fail to invest in trainings. Your factory workers who had, over time, become better at using the machine you provided them with, left for their villages when you laid them off. When I want the shirt again later, you will either have to call the same workers back (but they might have other jobs now) or you will have to hire new workers.

Since you have not had revenue during the lockdown, you might not have the money to train new workers. Hence, your ability to produce shirts of the same quality, at the same price in the same initial quantity might be permanently destroyed. If you are tired of words, take a break and watch the Harvard Business Review explain what shapes economic recovery can have.

We will be pretty unhappy in 2020-21

Given it took 10 years to grow at the same level as 2007 during our previous period of low growth, it is hard to be optimistic about the impact of COVID-19 on the Pakistani economy. But there are optimists out there.

The Finance Ministry of Pakistan is historically optimistic. When I started reading the Economic Survey of 2018-19, I saw growth slowing down from 5.5% in 2018 to 3.3% in 2019 and was unhappy. Then they revised figures and I found out growth had actually already slowed down to 1.9% in 2019. When they published their forecast of a contraction of 0.4% in 2020 vs. the initial IMF projections of 1.5%, I just shrugged. IMF had used inflated figures from the year before in their projections so the actual decline was almost the same as they had predicted. Next year the Ministry is predicting a V shaped recovery with growth of 2.1% while the IMF has a more realistic projection of 1.0%

Considering the lack of investment in Pakistan, the slowing down of real growth, the low levels of improvement in labor, capital and total factor productivity – it is just as difficult to see growth not being as low as what the IMF has predicted, as it is hard to believe that recovery will be V-shaped.

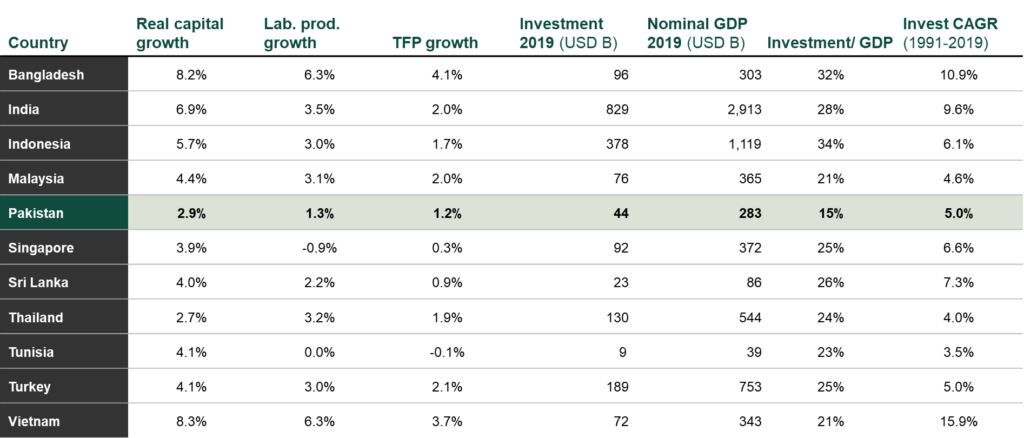

To understand my lack of optimism, compare Pakistan’s investment levels of 15% of GDP to other countries on the right side of the table below:

Global comparison of Investment as % of GDP

We reap what we sow

If you remember, consumption in our economy has been growing faster than the GDP growth rate of 5.7% since 1991. Investment on the other hand, has been growing slower. Again, compare us to Bangladesh, which has investment levels more than twice as high as Pakistan’s. As a result, their real capital has increased by 8% vs. our 3%, labor productivity increased by 6.3% vs. our 1.3% and total factor productivity increased by 4.1% vs. our 1.2%.

We will spend a lot of time later analyzing exactly where we have failed to invest and what the impact on our productivity has been but for now, let us explore how all these years of limited investment will affect us with COVID-19.

Real time data to predict GDP performance in Pakistan is quite limited.

Pakistan’s Large Scale Manufacturing (change between March 2019 and 2020)

However, the Large Scale Manufacturing Index, which shows the real growth in select industries in Pakistan, is published on a monthly basis. If you compare the March 2020 figures to March 2019 figures, you will see a contraction of 23%, which starts to paint a pretty bleak outlook. Textile and Food & Beverages industries, which make up the highest shares in the index, contracted by 26% and 21% respectively.

Not only is manufacturing expected to contract further, since it is the highest tax paying sector in Pakistan, government revenues are expected to decline too. All this while government expenses are supposed to increase with the alleged PKR 1.2 trillion package offered to Naya Pakistan.

They don’t care for us

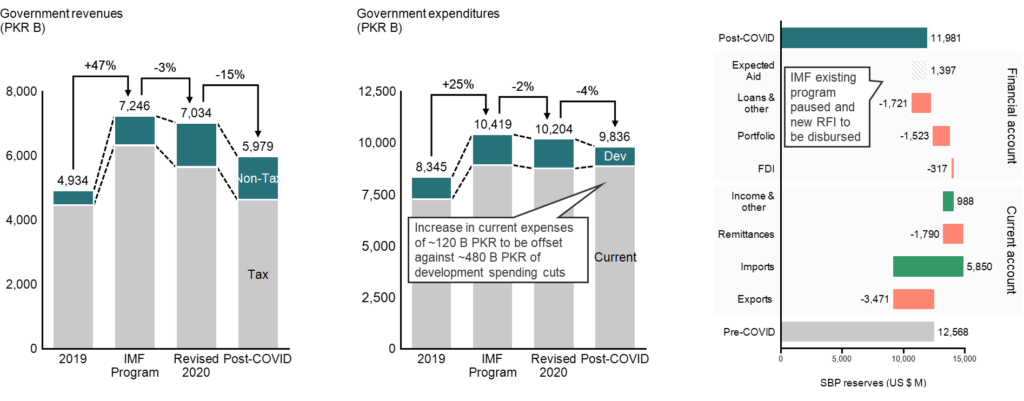

Impact of COVID-19 on Government revenues, expenses and foreign reserves

We are going through an IMF program right now, so that provides us a decent source of data too. How it works is that Pakistan enters a program and agrees on targets for a few metrics. Then, we start the year and soon realize those targets we set are unrealistic and would not be met, so, we get them revised. Then COVID-19 hits and we get them revised further. It is almost certain that we will not meet these targets either, but, at least we get to see some numbers and understand.

Government revenues are expected to contract by 15% versus the initial revised target while expenses will be cut by 4%. We will go into details of this later but it is important to notice that the government has made sure the number of PKR 1.2 trillion is on every citizen’s mind while there is no mention of the PKR 480 billion drop in development spending or public investment (shaded blue in the middle graph) which is also expected in 2020.

If you looked at the earlier version of the budget document released by the government, you would have seen that the revised development spending numbers for 2020 were actually omitted on purpose. Interestingly, the increase in current expenses (G) is only expected to be PKR 120 billion vs. the publicized figures. But don’t worry, since we will get a chance to dissect this later.

Some things should make us happy

There is a silver lining though.

Since we will have even less non-existent income to consume foreign goods, and unlike the 2008 financial crisis, this time oil prices have fallen to all-time lows for completely separate geo-political reasons, our dollar balance will not be worse off. To understand the dollar balance, let’s break it down into more digestible pieces.

Pakistan imports goods and services and needs to pay US dollars for them. Some of this currency comes from our exports to foreign countries and some comes from the remittances that non-resident Pakistanis send back home. But remember, we have been borrowing to make up for our non-existent income in the past from other countries, so we have to pay interest on them too. All these items broadly make up the current account portion of our dollar balance with the State Bank of Pakistan.

As discussed, this needs to be financed by the rest of the world, which is included in the financial account. Foreigners could give us money by directly investing in projects in Pakistan (FDI), buying stocks on the Pakistan Stock Exchange or buying bonds that are used to raise debt (portfolio investment). Alternatively, the government could directly take a loan from a country or from an agency like the IMF.

Pre-COVID-19, the State Bank had US$12.6 billion in their reserves and as you can see in the graph, this number is expected to be maintained post the pandemic. There is a lot of orange which shows we will be worse off due to reduced exports, remittances, FDI and portfolio investment since the outside world is contracting and not willing to lend as many dollars to us as before.

However, there are two significant green blocks too. Pakistan will benefit from almost US$6 billion fewer imports since Pakistanis do not have as much money to spend on foreign goods and services as before (demand shock) and oil prices have fallen sharply (supply shock).

At the same time, we will pay lower interest on our existing loans since we have received some debt relief from the IMF and at the same time, global interest rates are also at an all-time low. We will discuss all of this in detail later but for now, understand that on at least one front, we will not be as adversely affected by COVID-19 as on other fronts.

We were already on shaky ground

All countries will be impacted by COVID-19 in 2020 so it is actually more important to focus on what we need to do to recover. It is of utmost importance to avoid permanent damage to the economy which will limit our ability to grow, which has been the case in the past. We will focus on the more detailed impact on employment, government spending, trade and GDP later.

For now, the major takeaway should be that Pakistan’s economic contraction was already forthcoming given the decline in 2019. Our high levels of consumption combined with low levels of investment were leading to low productivity, and hence, higher prices. However, declining imports are expected to mitigate some of the immediate damage.