SBP’s new autonomy and targeting inflation

Oil prices in Pakistan are particularly relevant to consumer spending in the country. Based on the Consumer Price Index basket, approximately 10% of total consumer spending in Pakistan comprises of oil and related products. This includes commodities like electricity, gas, and motor fuel. Furthermore, oil prices also have the ability to affect inflation through a rise in production and distribution costs. Under the proposed amendments in the existing State Bank of Pakistan (SBP) Act, the SBP’s primary role will be domestic price stability, which would be achieved by targeting inflation. In that case, the State Bank’s monetary policy response would be dependent on inflation deviating from its target. Since the SBP’s monetary policy reaction function is likely to rely on inflation moving forward, it is worth exploring how oil prices in Pakistan affect inflation

Approximately 10% of consumer spending in Pakistan comprises of oil and related products

Weight of different commodities in CPI basket

| Base year 2007-08 | National |

| Food and Energy | 45.25 |

| Food | 36.25 |

| Electricity | 4.40 |

| Gas | 1.58 |

| Motor Fuel | 3.03 |

| Core (Non-Food and Non-Energy) | 54.75 |

| Total | 100.00 |

Source: Pakistan Bureau of Statistics and author’s calculation.

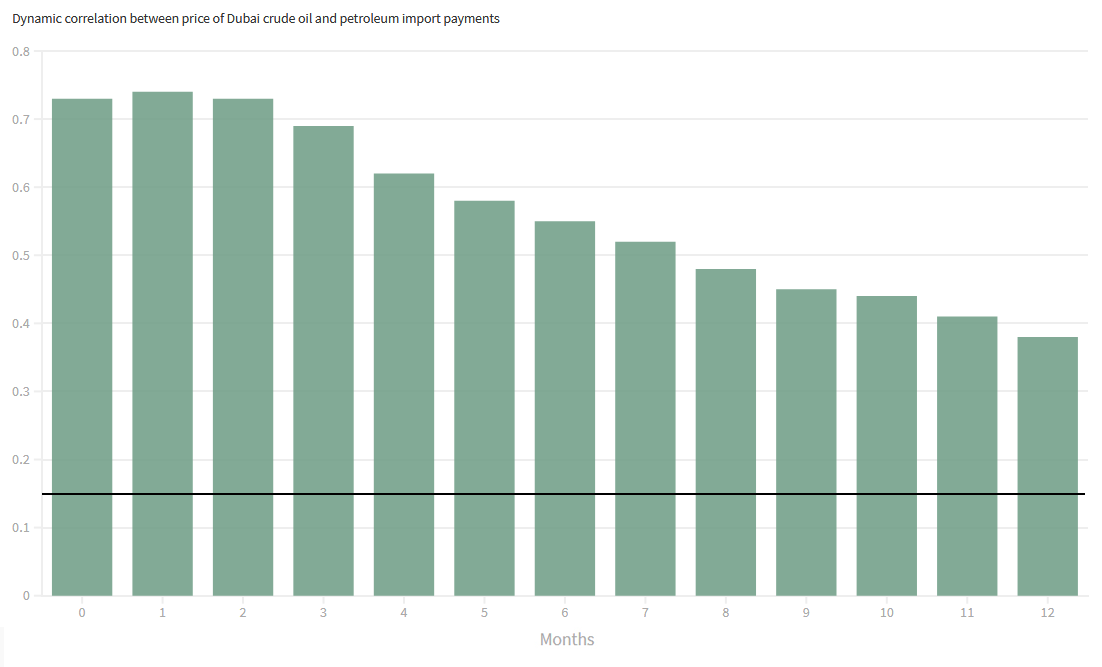

Between January 2010 and December 2020, the share of oil products in Pakistan’s total import bill was 28.47% on average. This meant that any fluctuations in oil prices would have significant implications for Pakistan’s import bill. The chart below shows a positive and significant correlation between the price of Dubai crude oil, and the current/lead values of petroleum import payments. This suggests an increase (decrease) in oil prices leads to an increase (decrease) in import payments on petroleum products in the short to medium-run. The strong correlation with the lead values means that the impact of a change in oil prices on petroleum import payments can be felt in the same month, and even up to a year.

Impact of change in oil prices on petroleum import payments can be felt for up to a year

Source: U.S. Federal Reserve Economic Database and Karandaaz Data Portal

Identifying the source of the oil price shock

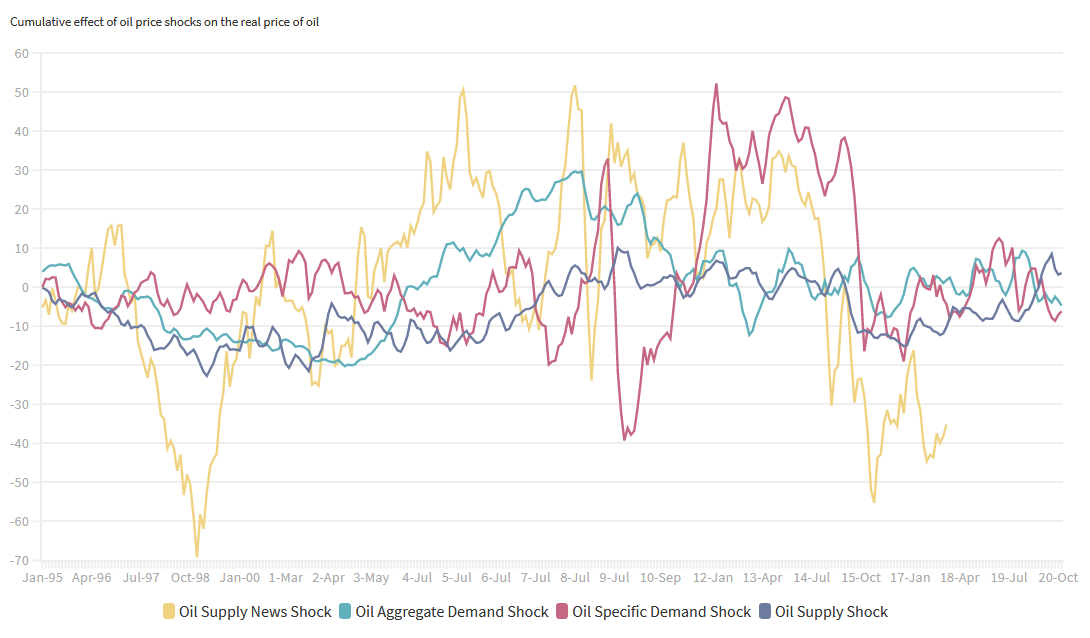

Before we examine the response of inflation to oil prices in Pakistan, it is imperative to identify the source of change in global oil prices, i.e. whether price change is driven by a supply or demand shock. This article focuses on the oil specific demand and oil supply news shock that are collectively responsible for 90% of fluctuations in global oil prices over the last 25 years. In doing so, factors like change in oil prices due to varying global aggregate demand or global crude oil production are left out since their impact is not as important.

Oil price fluctuations are driven by oil specific demand or oil supply news shocks

Source: U.S. Energy Information Administration, U.S. Federal Reserve Economic Database, Kanzig (2021), and author’s calculation

Oil-specific demand shock, derived following Kilian (2009), refers to a change in the price of oil driven by an increase in demand for oil due to expectations of shortfall in future oil supplies. For example, this shock can be thought of capturing an increase in the price of oil driven by an increase in demand for oil. This could be due to skepticism about future oil supplies as war and conflict breaks out in the Middle East. On the other hand, the oil supply news shock by Känzig (2020) identifies variation in oil prices around OPEC’s production announcements. For example, this shock captures an increase in oil prices if OPEC announces a reduction in overall crude oil production. A recent example of this was during the 13th OPEC and non-OPEC Ministerial Meeting in January 2021. This announcement eventually led to an increase in oil prices.

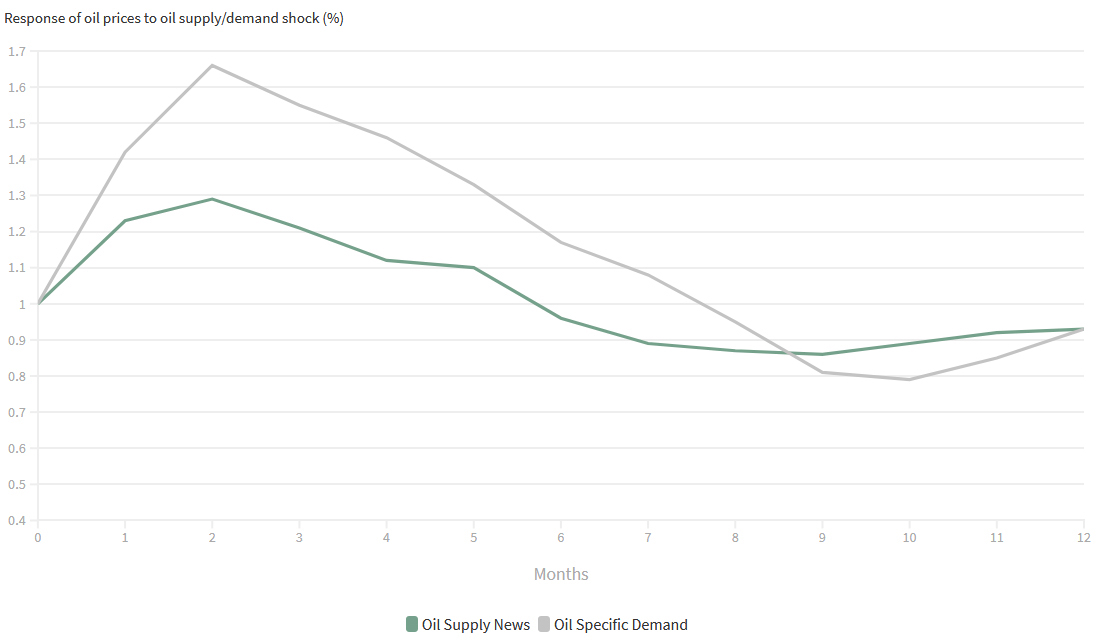

Most oil price fluctuations from February 1994 onwards were driven either by the oil-specific demand or oil supply news shocks. While the oil aggregate demand shocks played a pivotal role in driving up the price of oil before the 2007-08 Global Financial Crisis, its importance in recent years has diminished considerably. Chart below presents the response of Dubai crude oil price to each kind of oil price shock. Following an oil-specific demand shock, oil prices increase by 1% on impact and by 0.93% over the course of a year. The response to an oil supply news is also similar, with the year-long impact suggesting a 0.93% increase. These results indicates that supply or demand driven oil price shocks have a permanent effect on oil prices in Pakistan.

Both supply and demand driven oil price shocks have a permanent effect on price of oil in Pakistan

Source: Author’s calculations

How oil prices are set in Pakistan

The Economic Coordination Committee (ECC), on recommendation of the Oil and Gas Regulatory Authority (OGRA), usually controls petroleum prices and decides the pass through of global oil prices to domestic ones. Whenever there is a change in oil prices, the ECC has the following three options:

- If oil prices increases, the ECC could limit the pass through of oil prices to domestic consumers by giving subsidies. This will most likely have an adverse impact on the fiscal balance if taxes are not raised to finance this subsidy.

- If oil prices decrease, the ECC could decide against reducing domestic oil prices. It could keep prices at the same level, and instead impose additional levy to raise revenues. An increase in revenue will improve the fiscal balance.

- If oil prices change (increase or decrease), the ECC could allow for a complete pass through (increase or decrease) to domestic consumers and adjust domestic prices accordingly.

In addition to the fiscal priority, the ECC’s reaction function also depends on previous inflation.

- If inflation in the previous month is higher than expected inflation, the ECC might give a subsidy to reduce the burden on domestic consumers as global oil prices increase. On the other hand, if oil prices decrease, the ECC could allow for a complete pass through and reduce domestic oil prices.

- If inflation in the previous month is lower than expected inflation, the ECC could allow for a complete pass through of an increase in global oil prices to domestic oil prices. On the other hand, if global oil price decreases, the ECC could decide against reducing domestic oil prices and use this opportunity to raise revenue by imposing a levy.

It is worth noting that a more recent example of the ECC not responding to global oil price changes was during the COVID-19 pandemic. The drastic fall in demand delivered a significant blow to the global crude oil market and pushed oil prices to multi-decade lows. However, the ECC decided against transferring the entire decrease in petroleum prices and instead increased the levy to improve the fiscal balance.

Headline vs. Core inflation response

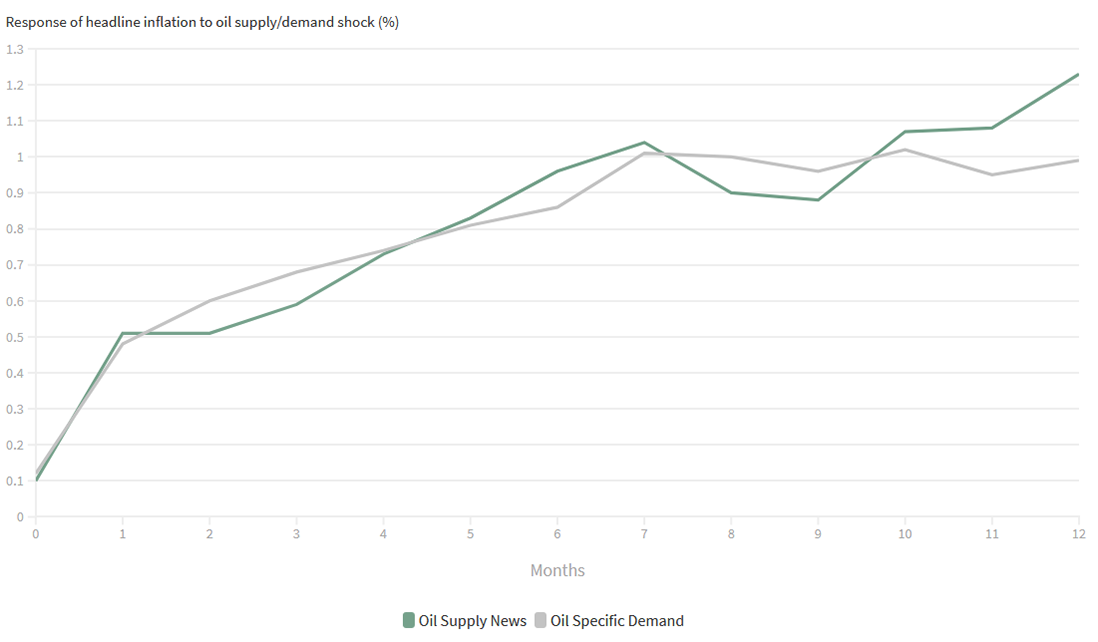

The estimated response of headline inflation to oil price shocks on monthly data from 1994 to 2020 is presented below. These responses are expressed in annualized terms. Movements in inflation due to real exchange rate depreciation and ECC’s pass through mechanism are controlled for in the econometric specification. An oil specific demand shock that increases oil price by 0.93% over the course of a year, leads to an increase of 0.99% in overall prices. Furthermore, an oil supply news shock that increases oil prices by 0.93% over the course of a year results in an increase of 1.23% in the overall price level. These results point to the importance of understanding the source of the oil price movement since the magnitude of headline inflation is likely to differ depending on whether the shock is supply or demand driven.

Oil supply news shocks impact headline inflation by a larger magnitude vs. demand shocks

Source: IMF International Financial Statistics and author’s calculation

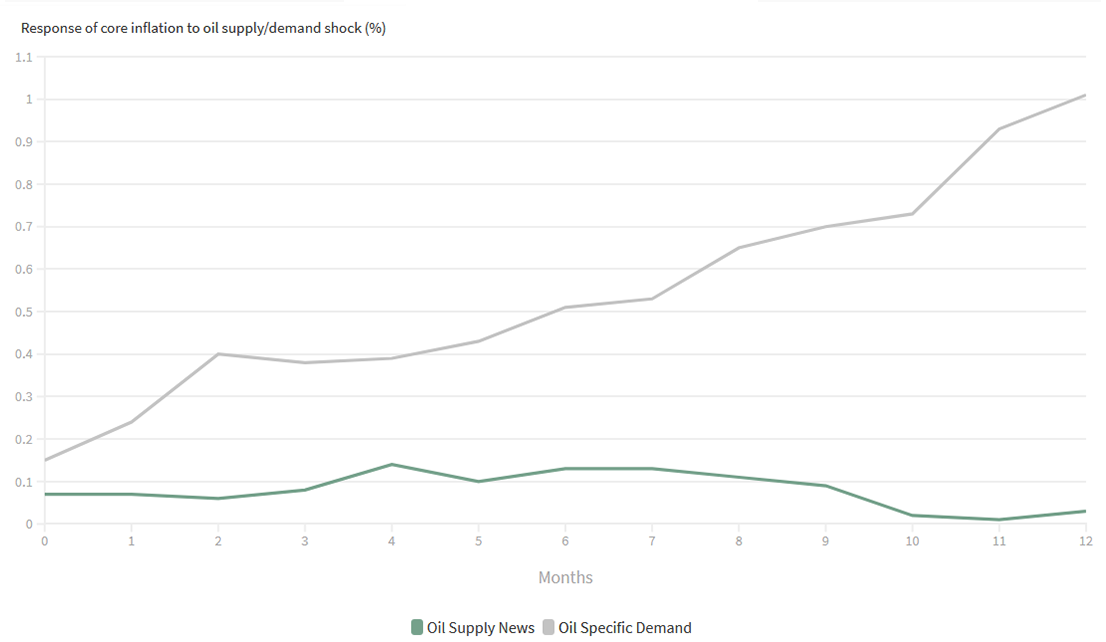

While headline inflation responds strongly to oil price shocks, it is worth exploring how Core (Non-Food and Non-Energy) inflation behaves. After all, core goods and services comprise 55% of consumer spending as mentioned earlier. The impulse responses in above can be interpreted as a combination of food and energy inflation and core inflation responses to oil price shocks. As a result, core inflation impulse responses will give us an idea of which commodity group is responsible for driving headline inflation. Chart below presents the responses of annualized core inflation to oil price shocks. Core inflation increases by around 1.01% over the course of a year following an oil specific demand shock. Since the response of headline inflation is known, the imputed response of food and energy inflation to an oil specific demand shock is estimated to be around 0.97%. In this case, both commodity groups are almost contributing equally to headline inflation. As for the oil supply news shock, the response of core inflation is very small. Consequently, it can be concluded that the response of headline inflation to oil supply news shocks is driven primarily by food and energy inflation.

Oil supply news shocks have a very small impact on Core (Non-Food and Non-Energy) inflation

Source: Karandaaz data portal and author’s calculations

SBP’s monetary policy reaction function

Scenario 1: SBP targets headline inflation

Based on the Forecasting Policy Analysis System (FPAS) model developed by Shahzad and Pasha (2015), oil price shocks are likely to have an impact on future inflation through the expectations channel. This suggests that global oil price shocks increase current headline inflation, which in turn leads to expectation of higher future inflation. Consequently, a forward-looking State Bank would respond by raising the policy rate. However, if oil price shocks have asymmetric effects on the magnitude of headline inflation (as shown earlier), one would expect the State Bank’s monetary policy reaction function to account for this, and change the policy rate accordingly. For example, headline inflation increases by a larger magnitude following an oil supply news shock in comparison to an oil specific demand shock. As a result, the rate increase following an oil supply news shock would also be larger.

Scenario 2: SBP targets core inflation

There is strong precedent of central banks across the world, like the U.S. Federal Reserve, using core inflation as the target to vary the policy rate since it exhibits a much lower degree of volatility than headline inflation. If the State Bank of Pakistan does respond to core inflation, there are important lessons to be learned from the estimated asymmetric effects of oil price shocks. The oil specific demand shock leads to headline inflation, which is driven by both commodity groups, i.e. food and energy, and core. Since core inflation is responding to an oil specific demand shock, the State Bank of Pakistan could respond by raising the policy rate. However, with the oil supply news shock, headline inflation is driven primarily by food and energy inflation, and not core. Since control of food and energy prices comes under the Government of Pakistan, it would not be viable for the State Bank of Pakistan to respond to oil supply news shocks by raising the rate.

Recommendation

Since each kind of oil price shock has an asymmetric effect on inflation, it is important to decompose oil price movements into the respective supply and demand component. Anticipating the source of the oil price shock before time is essential in determining the optimal monetary policy response of the SBP to oil price shocks. A credible and forward-looking SBP, which will be responsible for meeting its respective inflation target in the near future, could forecast the source of oil price shocks by applying a mix of actual and forecasted data for variables like global crude oil production, real economic activity index and the real price of Dubai crude oil, to the econometric specifications of Kilian (2009) and Känzig (2020). Doing so, would allow the SBP to devise its policy rate in a way that it is able to meet the inflation target.

One Comment